'/%3e%3cpath%20d='m711.6%20144%2036-36-36-36a71.9%2071.9%200%200%200-62.3%2036%2071.9%2071.9%200%200%200%2062.3%2036z'%20class='st2'/%3e%3cpath%20d='M44.5%2063c11.3%200%2021.2%205%2026.5%2017.1%205.8-11%2016.9-17.1%2029-17.1%2022%200%2031.9%2015.7%2031.9%2034.7v52.9H115v-47.3c0-13.9-4.1-26.1-18.9-26.1-15.5%200-21.6%2014-21.6%2027.4v46.1H57.4V99.9c0-13.3-4.5-22.7-18-22.7-12.4%200-21.8%2011.2-21.8%2028.1v45.4H.7v-67c0-4.5-.2-12.8-.7-18.4h16c.4%204.3.7%2010.4.7%2014h.5C21.6%2070.4%2031.5%2063%2044.5%2063zM200.7%20153c-26.1%200-45.9-18.9-45.9-45.2S174.6%2063%20200.7%2063c26.1%200%2046.1%2018.5%2046.1%2044.8s-20%2045.2-46.1%2045.2zm0-76c-18.2%200-28.4%2014.6-28.4%2030.8%200%2016.2%2010.3%2031%2028.4%2031%2018.4%200%2028.4-14.8%2028.4-31S219.1%2077%20200.7%2077zM285.5%2065.3c.4%204.3.7%2010.4.7%2014h.5c4.1-9.2%2015.5-16.4%2027.7-16.4%2022%200%2031.9%2015.7%2031.9%2034.7v52.9h-16.9v-47.3c0-13.9-3.8-26.1-19.4-26.1-13.3%200-22.9%2011.2-22.9%2028.1v45.4h-16.9v-67c0-4.5-.2-12.8-.7-18.4h16zM383.6%2045.4c-6.1%200-11.2-4.9-11.2-10.8%200-6.1%205-11%2011.2-11s11.3%204.7%2011.3%2011c0%206.1-5.2%2010.8-11.3%2010.8zm8.4%20105.3h-16.9V65.3H392v85.4zM463.3%2079.2h-22.7v44.5c0%2010.3%203.6%2014.4%2012.1%2014.4%203.1%200%207-.7%209.9-2.2l.5%2013.9c-4%201.4-9.2%202.3-14.4%202.3-16%200-24.8-9-24.8-26.6V79.2h-16.4V65.3h16.4V40.9h16.7v24.5h22.7v13.8zM521.1%20153c-26.1%200-45.9-18.9-45.9-45.2S495%2063%20521.1%2063c26.1%200%2046.1%2018.5%2046.1%2044.8s-20%2045.2-46.1%2045.2zm0-76c-18.2%200-28.4%2014.6-28.4%2030.8%200%2016.2%2010.3%2031%2028.4%2031%2018.4%200%2028.4-14.8%2028.4-31S539.5%2077%20521.1%2077z'%20class='st3'/%3e%3c/svg%3e)

Best Online Banks in Europe in 2024: Fees, Features, and More

Byron Mühlberg

Guide

Jarrod Suda

Reviewer

By offering low fees, easy application, and convenient web and mobile apps, online banks have risen rapidly in prominence across the EU in recent years, going even so far as to challenge traditional banks for a new tech-savvy generation of customers.

In 2024, as both the popularity and the market share of Europe's online banks continue to rise, you might wonder which of the many online banks in Europe offers you the best service. In this guide, we whittle down the top online banks in the EU/EEA fintech scene to the prominent contenders and explore which one might make sense for you.

Authorized as an electronic money institution across the EU, Revolut provides money accounts with an EU IBAN, debit cards, and multi-currency features. Additional services like trading, lending, and savings products are also offered. Revolut provides a useful account option with no monthly account maintenance fees charged. ✨ Get three months of free Revolut Premium as a Monito reader with our exclusive link.

How Monito Scores Online Banks in Europe

To determine which online banks scored better than others within the EU/EEA market, we used a consumer-first framework to analyse several key factors. To begin with, we weighed a number of concrete metrics relating to factors such as fees and rates, ease of use, credibility, service and coverage, transparency, and customer satisfaction to piece together a reliable all-around picture of which top digital banks offer the savviest solutions to EU residents.

Next, we explored these results and presented our findings in the form of a series of key takeaways that we believe you should know about the three digital banks ranked highest.

In our definition of "online bank," we only consider:

- Digital banks that are available across all or most EU/EEA countries, not just in specific countries.

- Online-first banks, and not traditional banks which have pivoted to digital banking while still maintaining an extensive brick-and-mortar infrastructure.

While we ranked these online banks on an overall list, bear in mind that this list does not mean that our choice for the EU's best digital bank is necessarily the best choice for you. As you'll see, each online bank comes with its own unique set of pros and cons that may impact its overall relevance to you.

If you'd like to see how EU online banks stack up against one another, then check out our live neobank comparison engine.

Without further ado, let's go through our rankings for the top online banks in Europe in 2024 —

Best Online Banks in Europe

Key Facts About Best Banks For a Euro Account

| 👥 No. of customers | ≈ 50 million |

|---|---|

| 🔎 No. reviewed on Monito | 10+ |

| 💸 Average monthly fee | €0.00 |

| 🏆 Best overall | |

| 📶 Largest (customers) | |

| 📶 Largest (revenue) |

Revolut: Best All-Rounder Euro Account

A major name in financial technology, Revolut has been at the forefront of Europe's online financial services sector in recent years. With over 12 million users, the London-based company is available not only in the EU and EEA but worldwide. However, because it operates as an electronic money institution rather than a bank in most countries, Revolut may serve as a complementary spending tool alongside a primary bank account.

- Account Name: Standard

- Account Details: Lithuanian IBAN, UK account number

- Licensing: Bank

- Account Maintenance: €0 /month

- Noteworthy Features: UK bank account details, multi-currency balances, trading, savings, tracking and analytics.

- Availability: 30 European countries

- Overview of All Plans:

Account Name | Fee /Month |

|---|---|

0 | |

3.99 | |

8.99 | |

15.99 | |

55 |

- More Info: See our full Revolut review or visit the website.

Revolut Bank UAB offers banking services in parts of the EU/EEA (including in France, Italy, Portugal, Estonia, Greece, Latvia, Romania, and a few others), while Revolut's global services operate under e-money licenses. Services may vary by entity, including deposit protections and insurance.

However, whether you choose Revolut or Revolut Bank, the platform offers a range of financial services typical of traditional banks, making it an attractive alternative to high-street banks due to its unique ability to offer low fees and impressive scope of service.

Opening up a 'Standard' account with Revolut is completely free, but delivering the first debit card will set you back around €5. ATM withdrawals have no Revolut fees up to €200 per month, beyond which a 2% Revolut fee applies per withdrawal. Moreover, transferring money to other Revolut users is free and instant. This makes the service a reliable choice if you frequently send money to other Revolut users.

In addition, Revolut offers low fees on international money transfers, making the service an attractive choice for those who frequently send money across borders. They charge no exchange rate margins on weekdays, with users only subject to a flat 0.50% fee on all transfers sent abroad. However, be aware that Revolut charges twice the fee for international money transfers made on weekends — bumping the fee to 1% on Saturdays and Sundays.

Revolut Advantages

- An extensive range of financial services,

- The debit card is well-priced for international spending,

- Includes investment functionality,

- Slick mobile app with many features,

- Foreign transactions up to €1,000 (or equivalent) have no FX fees charged by Revolut Monday-Friday. Surcharges and limits apply.

Revolut Disadvantages

- Access to some interesting perks is restricted to 'Standard' users,

- Many foreign currency transactions incur a fee,

- Higher currency conversion costs on weekends.

In the end, Revolut provides useful spending features alongside a primary bank account. It is ideal if you'd like to cut down on the high fees associated with basic banking services at high-street banks and is particularly well-suited for travelling abroad, especially if you plan to spend less than €1,000 (or equivalent) and do most of your spending on weekdays. It's for all these reasons that we rate Revolut as the best all-rounder online bank in the EU.

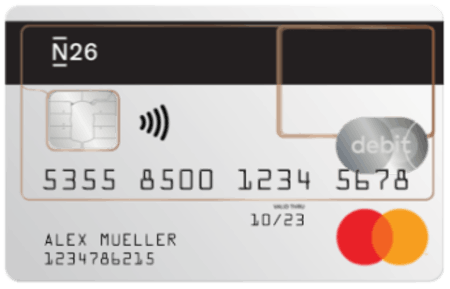

N26: Best Free Current Account

Arguably the best-known mobile bank, N26 is a widely-used and much-loved German online bank with around seven million customers across the EU. N26 is also partnered with Wise's money transfer service, allowing in-app international money transfers at some of the best exchange rates on the market. Because of its complete current account offering, we recommend N26 to just about anybody interested in low-cost banking.

- Account Name: N26 Standard

- Account Details: German IBAN

- Licensing: Bank

- Account Maintenance: €0 /month.

- Noteworthy Features: Instant social payments, overdraft facilities, cash deposits

- Availability: 22 European countries

- Overview of All Plans:

Account Name | Fee /Month |

|---|---|

0 | |

4.9 | |

9.9 | |

16.9 |

- More Info: See our full N26 review or visit the website.

N26 offers several paid accounts and one free account, 'N26 Standard', which in our opinion is a very capable and complete online banking package in and of itself (especially considering it doesn't cost a cent in monthly fees). 'N26 Standard' is a fully-fledged current account available online and in the N26 app. It allows mobile payments and includes a transparent debit Mastercard, which arrives with no delivery fee.

While very cheap, there are some costs to consider when using the 'N26 Standard' account. For example, the account is free up to three ATM withdrawals per month in the Eurozone, after which it costs €2 per withdrawal. And, as mentioned above, cash withdrawals at ATMs outside the Eurozone (e.g. Switzerland, Norway, UK, US, etc.) come with a fairly steep 1.70% commission on the total amount withdrawn.

N26 Advantages

- Integrated with Wise for international money transfers;

- A secure current account with a licensed bank;

- Instant transfers to most other SEPA bank accounts;

- The standard plan is practically free for everyday use.

N26 Disadvantages

- A 1.70% fee for foreign currency ATM withdrawals;

- No interest, loans, joint account, or multi-currency functionality;

- Not available for UK residents or citizens;

- Upgrade needed for unlimited, fee-free cash withdrawals.

Upgrading plans with N26 can cost you between €4.90 and €16.90 and will bring you benefits such as comprehensive insurance, spending statistics, and preferential customer support. However, the core banking features of N26 are all available on the free account, and in our opinion, this account should give you everything you're looking for if free basic banking services are what you're after.

Living in Italy? N26 is unavailable there. See more.

Tomorrow: Best for Sustainability

Tomorrow is a fintech company affiliated with German bank Solarisbank striving for positive impact and claiming to put sustainability before profit. Customers can choose between three sustainable current accounts, the first two coming with a plastic Visa debit card, and the premium tier coming with a wooden Visa debit. We particularly think Tomorrow's basic 'Now' account is the ideal choice for sustainability-oriented customers due to its low all-around costs and pro-sustainability investments.

- Account Name: Now

- Account Details: German IBAN

- Licensing: Payment Institution

- Account Maintenance: €3-€9 /month

- Noteworthy Features: Climate contributions, savings pockets

- Availability: 4 European countries

- Overview of All Plans:

- More Info: See our full Tomorrow review or visit the website.

All three of Tomorrow's paid account models (which range from €3 to €15 per month) create sustainable investments. This is achieved using transaction costs and user deposits, which are partly invested in projects such as afforestation, sustainable energy production, or drinking water purification in poorer regions of the world.

Tomorrow Advantages

- Customer money is invested in sustainable projects;

- Good checking account for everyday use;

- Attractive pricing for foreign currency transactions;

- Interesting perks, including community pockets and Tomorrow Funds;

- Stylish debit card in an artistic design.

Tomorrow Disadvantages

- Starts at €3 per month in account management fees;

- Not available for UK residents or citizens;

- Cash withdrawals can be pricey;

- Missing cash deposits, international transfers and other core features.

Even with Tomorrow's base account, the CO2 footprint of the account holder is compensated, and with its premium 'Zero' account, the package comes with a debit card made of wood, which is a unique perk that allows your card to stand out visually from the rest.

Aside from its focus on sustainability, Tomorrow also has a lot to offer functionally. The platform enables free payments worldwide and offers currency conversion at the mid-market exchange rate with both account models. Cash withdrawals abroad on the free account cost 1.5% of the withdrawal amount.

We are particularly interested in the fact that Tomorrow offers an excellent user experience despite its sustainable approach and stands out with attractive fees for use at home and abroad. Thus, you won't have to compromise when receiving a sustainable current account with excellent functionality and low transaction costs.

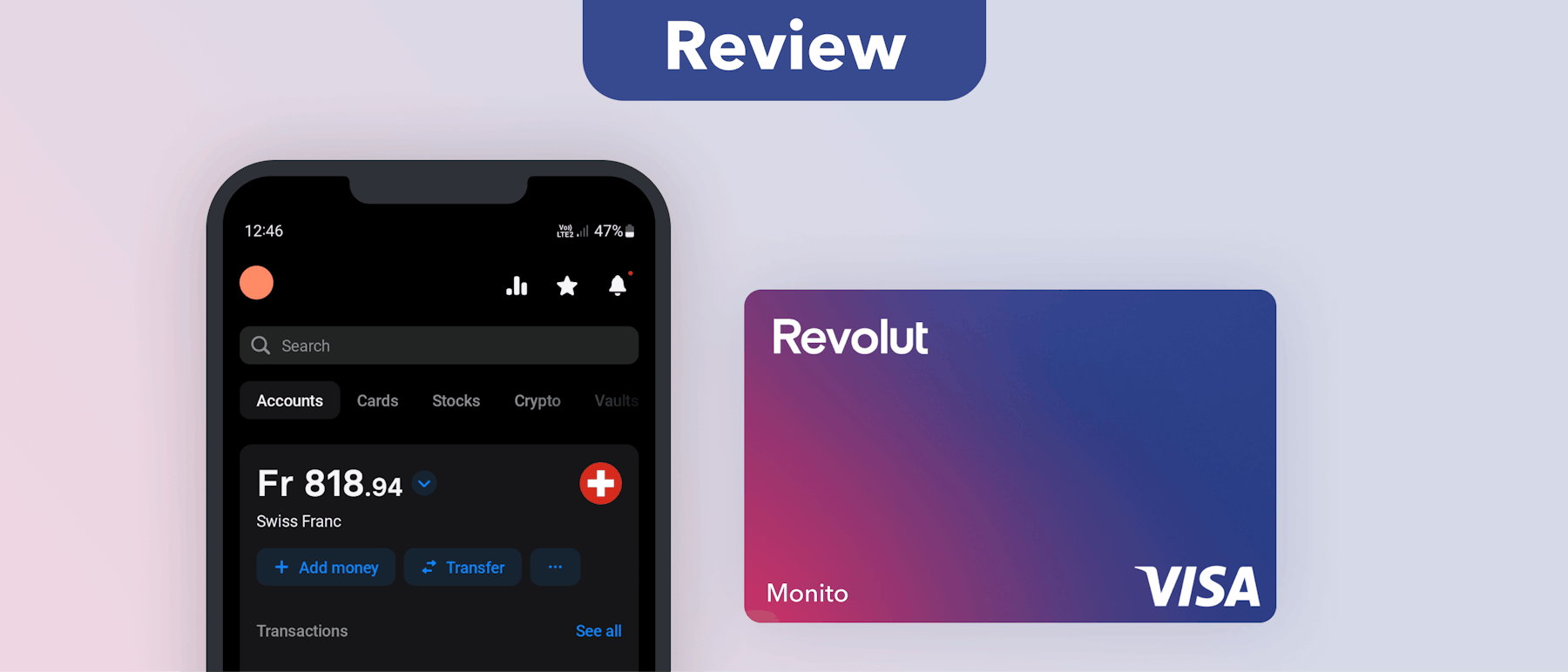

Wise: Best Multi-Currency Account

Wise is not a bank but a money transfer operator well-known for offering some of the cheapest international transfers globally. (In fact, according to our rankings, Wise is the best money transfer service.) However, money transfers aren't Wise's only game; they also offer the Wise Multi-Currency Account — a low-cost foreign currency spending account and card product that's best in class on the market.

- Account Name: Multi-Currency Account

- Account Details: Belgian IBAN and 9 others

- Licensing: Payment Institution

- Account Maintenance: €0 /month.

- Noteworthy Features: International money transfers, multiple account details, multi-currency balances, virtual debit cards.

- Availability: 32 European countries

- More Info: See our full Wise Account review or visit the website.

Wise in Short

Applying for a Wise Account is fast and easy and can be opened while abroad and done using proof of residence in the EU/EEA (as well as many countries worldwide). Once you're signed up and your card has arrived (which takes up to two weeks in Europe), you'll be able to take advantage of the following unique features with the account:

- Local bank details in the US, Eurozone, UK, Australia, New Zealand, Singapore, Romania, Canada, Hungary, and Turkey;

- Hold, exchange, and top-up up to 56 currencies;

- A multi-currency Visa debit card that's handy for paying in foreign currencies without the hidden fees;

- Access to Wise's powerful international money transfer service right from your account balance.

![]()

Wise Advantages

- Account details in as many as 10 currencies;

- Hold money in 50+ currencies;

- Send money to 80+ countries from your account;

- Some of the lowest money transfer fees available on the market;

- Pricing is accessible and transparent;

- Mid-market exchange rate offered for currency transfers;

- Wise card can be used to avoid foreign transaction fees;

- No setup fees or monthly charges.

Wise Disadvantages

- Cash or cheque payments aren't supported;

- Overdraft and loans aren't available;

- Negative interest on large Euro account balances;

- Fees to top up the account via debit and credit card;

- Tight limits and conditions to fee-free ATM withdrawals.

How Wise Works

To get a sense of just how useful Wise can be for frequent travellers and expats, let's say that you've just moved from the UK to Portugal and you'd like to spend in Euros before you've got your proof of residence sorted out. With the Wise Multi-Currency Account, you'll be able to:

- Send British pounds from your bank account to your Wise Euro account;

- Convert to Euros at a low fee (e.g. if you add €1,000 and pay with British pounds, the total fee will be around 0.35% or £3);

- Pay with your Wise debit card, make or receive SEPA (and SWIFT) payments, and set up direct debits.

You'll also have a dedicated set of Belgian bank details to share with a European employer. Belgian IBANs are fully eligible in the Eurozone, and rejecting the payout or receipt of funds based on the origin of an IBAN is illegal. Note that this account does not offer an overdraft, and you won’t earn interest on any in-credit balances.

Final Word

For the above reasons, we think Wise is the best online multi-currency account available to Europeans and a product we firmly recommend for holidaymakers, online spenders, and expats alike.

Bunq: Best Paid Current Account

Dutch neobank bunq doesn't really lift a candle to some of the other contenders on this list in terms of affordability. That's because bunq doesn't offer a free account, and many of its services come with additional fees. However, for those who don't mind paying higher fees every month for an online bank account, then bunq comes packed with many interesting features and perks to take advantage of.

- Account Name: Easy Bank

- Account Details: Dutch bank account

- Licensing: Bank

- Account Maintenance: €2.99 /month.

- Noteworthy Features: Bill splitting, Wise money transfer integration,

- Availability: 27 European countries

- Overview of All Plans:

Account Name | Fee /Month |

|---|---|

0 | |

2.99 | |

8.99 | |

17.99 |

- More Info: See our full bunq review.

Available in most EU/EEA countries, bunq offers three different bank account types priced between €2.99 and €17.99 per month. Following a major pricing update in 2021, bunq went from being one of the cheapest neobanks for overseas spending to one of the most expensive. On bunq's most affordable plan, card spending in foreign currencies while abroad incurs a 1.5% commission on the transaction amount as well as a 0.5% network fee, while on the two more premium plans, the 1.5% commission is waived for cashless payments abroad, but the 0.5% network fee remains.

Cash withdrawals are also rather pricey at bunq, regardless of the plan. On the cheapest 'Easy Bank' plan, not only does the €0.99 per withdrawal fee apply for the first four withdrawals per month (after which the fee bumps up to €2.99 per withdrawal), but these come in addition to the 1.5% commission and 0.5% network fee for foreign currency withdrawals. This means that for a $1,000 withdrawal in the US, you'd pay 2.1% in fees, which is comparable to the fees charged by traditional banks.

Despite the pricing update, whether you're an expat, a frequent traveller, or a digital nomad, you'll find bunq to still be, on average, a cheaper option for overseas spending than traditional banks, though, although not quite as cheap as come of its major alternatives such as N26 and Revolut.

Bunq Advantages

- The choice between a Spanish, German, French, or Dutch IBAN;

- Partnered with Wise for international money transfers;

- A licensed bank in the Netherlands;

- Notifications and sub-accounts to manage spending;

- Built-in savings with interest.

Bunq Disadvantages

- No free plan is available;

- Climate contribution on 'Easy Green' plan is usually not worth it;

- Relatively expensive premium tiers;

- ATM withdrawals are pricey on all plans.

Bunq Plans

Bunq accounts break down into three tiers as follows:

- Easy Bank: A low-cost current account with a German, French, Spanish, or Dutch IBAN that comes with a debit Mastercard and money transfer capabilities. The account costs €2.99 per month.

- Easy Money: An account with added features and functionalities, including spending statistics, four free ATM withdrawals per month, budgeting features, unique deals, a metal debit card, and bookkeeping software. The account costs €8.99 per month.

- Easy Green: The premium tier, Easy Green's unique feature allows users to track the progress of the reforestation initiative already linked to other tiers (i.e. a tree planted for every €100 spent). Costing €17.99 per month, we've found in our bunq review that this initiative is not worth it for most users.

Because of the costs involved, we think bunq isn't suitable for all kinds of users, especially those looking to cut back on expenses or those who aren't necessarily looking for an eco-friendly solution in their bank. However, suppose you live in Spain, France, Germany or the Netherlands and want an IBAN for one of these countries (especially if you don't mind paying the €2.99 per month fee for the perks that bunq has to offer). In that case, we'd recommend bunq's 'Easy Bank' plan, which provides an interesting paid online bank account that will probably give you everything you're looking for and more.

Yuh: Best Swiss Franc Account

Yuh is a Swiss neobank that's backed by Swissquote and PostFinance. It offers a Swiss franc (CHF) IBAN account and multi-currency functionality that allows you to hold in-app balanced in up to 13 other currencies, including EUR, USD, and GBP. Yuh also comes with a built-in stock and crypto trading platform. Because it's available in Switzerland and all neighbouring EU/EEA countries, we think it's the best CHF account in Europe and an excellent way to hold a balance in the currency if that's something you find helpful.

- Account Name: Yuh

- Account Details: Swiss IBAN

- Licensing: Bank subsidiary

- Total Cost: €0 per month.

- Noteworthy Features: CHF bank account details, multi-currency balances, stock and cryptocurrency trading.

- Availability: 6 European countries

- More Info: See our full Yuh review or go to the website.

Swiss neobank Yuh is an excellent online account that gives you an app-based account and a debit card. Together, they make a savvy and capable spending tool, although it lacks card and cash top-up methods, direct debits, interest, and overdrafts. The account comes with a slick black prepaid debit Mastercard, which costs nothing in month-to-month fees:

Yuh

With Yuh, you'll be able to hold a bank account in Swiss francs (with a full-fledged Swiss IBAN) and balances in 12 other currencies (including US dollars and all the currencies of the EEA). Yuh also offers 'projects', which you can use to put money aside into dedicated account-like spaces to be saved for short-, medium-, and even long-term goals (with CHF, EUR, and USD balances all accruing interest).

Another major perk of Yuh is that, using the app, you can buy fractional shares for as little as CHF 25 (a very low barrier to entry) in over 200 blue-chip companies or invest in "themes" (e.g. vegetarian, pharma, cannabis, etc.) to which you want to expose your portfolio. Yuh also offers an automated investment feature where it allows you to choose how often and how much you want to invest, and it'll make the trades for you.

Yuh Advantages

- Clean and well-designed mobile app.

- Backed by PostFinance and Swissquote.

- Excellent in-app investment features.

- Nifty 'Pay a friend' feature for instant transfers between users.

- A small and straightforward 0.95% fee on currency exchange.

Yuh Disadvantages

- Only possible to fund the account by bank transfer.

- Few customers and reviews to date.

Compare Euro Accounts Online in the US & Internationally

Here's an overview of ways to open a euro bank account or Euro currency account online with fintech platforms as well as major financial institutions.

Provider | Coverage in the US | Coverage internationally | Currencies | |

|---|---|---|---|---|

Revolut | ✔ | UK, EU/EEA | 25+ | Visit |

Wise | ✔ | UK, EU/EEA, CA, AU, NZ, JP, SG, MY | 40+ | Visit |

HSBC | ✔ | Global | Varies by account type | Visit |

Citi | ✔ | UK, EU/EEA, JP & more | 16 | Visit |

PNC Bank | ✔ | CA, CN, DE, UK | 30 | Visit |

TIAA Bank | ✔ | Corporate only | Not disclosed | Visit |

Wells Fargo | ✔ | Corporate only | Not disclosed | Visit |

Payset | ✖️ | EU/EEA, SG, JP, HK, IS & 8 more | 38 | Visit |

Payoneer | ✔ | US, UK, EU/EEA, JP, CA, AU, SG, HK & UAE | 10 | Visit |

Paysend | ✖️ | UK, EU/EEA | 30+ | Visit |

Last updated: 8 January 2024

The Best EU Online Banks Compared

To wrap things up, let's take a look at how the product, service, and pricing of a few of the online banks we explored compare to one another in the EU and EEA. We've chosen to compare the standard plans of Tomorrow, Revolut, and N26 because of their similar all-round product offerings:

|  |  | |

Account | Standard | Standard | Now |

Monthly Fee | 0 | 0 | 0 |

Intl. Withdrawal Fee | 0.017 | 3% | 0.015 |

Intl. Transaction Fee | 0 | 0 | 0 |

Intl. Transfer Fee | 0.3%-2.8% |

| N/A |

Card Delivery Fee | 0 | 0 | 0 |

Contactless | ✔ | ✔ | ✔ |

Google Pay | ✔ | ✔ | ✔ |

Apple Pay | ✔ | ✔ | ✔ |

3D Secure | ✔ | ✔ | ✔ |

Deposit Options |

|

| SEPA transfer |

Overdraft | ✔ | ✘ | ✘ |

Platforms |

|

| Mobile |

Deposit Insurance | 100000 | 100000 | 100000 |

No. of Customers | 7 million | 15 million + | Approx. 70,000 |

Trustpilot | 3.3/5 | 4.3/5 | 3.4/5 |

Customer Service |

| 24h in-app live chat |

|

| Try N26 ❯ | Try Revolut ❯ | Try Tomorrow ❯ |

Last updated: 8 January 2024

FAQ About Opening a Euro Account Online

Why You Can Trust Monito

Our recommendations are built on rock-solid experience.

- We've reviewed 70+ digital finance apps and online banks

- We've made 100's of card transactions

- Our writers have been testing providers since 2013

Top EU Online Banks Tips & European Life Guides

Why Trust Monito?

You’re probably all too familiar with the often outrageous cost of sending money abroad. After facing this frustration themselves back in 2013, co-founders François, Laurent, and Pascal launched a real-time comparison engine to compare the best money transfer services across the globe. Today, Monito’s award-winning comparisons, reviews, and guides are trusted by around 8 million people each year and our recommendations are backed by millions of pricing data points and dozens of expert tests — all allowing you to make the savviest decisions with confidence.

![]()

Monito is trusted by 15+ million users across the globe.

![]()

Monito's experts spend hours researching and testing services so that you don't have to.

![]()

Our recommendations are always unbiased and independent.